Categories

Buying, Selling, Comparisons, CostsPublished October 27, 2025

The Ultimate 2025 Guide to Downsizing in Las Vegas: What to Keep, What to Sell, What to Expect

The Ultimate 2025 Guide to Downsizing in Las Vegas: What to Keep, What to Sell, What to Expect

You walk past three bedrooms you never use.

You write another check for landscaping you don't have time to enjoy.

Your utilities hit $400 in July. Your property taxes climb 3% again. The HOA sends another assessment.

Meanwhile, your home has quietly built $200,000 in equity.

The tension: Las Vegas homeowners are sitting on record equity while paying for square footage, maintenance, and costs they no longer need.

The shift: 2025 has delivered something rare—a balanced market with over 7,500 single-family homes for sale, 4+ months of supply, and a growing inventory of condos, townhomes, and single-story options in Henderson, Summerlin, and beyond.

The promise: This guide shows you how to convert that equity into a right-sized home, slash monthly costs by 30–50%, and navigate the sale, purchase, and move without losing control or money in the process. You'll see the numbers, the neighborhoods, the process map, and the exact resources that make 2025 the year to act.

Why 2025 Favors Downsizing in Las Vegas

Las Vegas Realtors (LVR) reports a housing market that has fundamentally shifted from the competitive, inventory-starved conditions of 2021–2023 to a balanced environment where buyers—including downsizers—now have leverage.

As of September 2025, the Las Vegas market reached 4+ months of housing supply, up from 2.9 months in September 2024. This represents a critical threshold: markets with 4–6 months of supply are considered balanced, meaning neither buyers nor sellers hold outsized negotiating power.

The inventory surge tells the story clearly. 7,502 single-family homes were listed without offers in September 2025—a 37.4% increase year-over-year. Condos and townhomes saw even steeper growth, with 2,605 units available, up 50.5% from the previous year.

For downsizers, this translates to selection. You're no longer competing against five other offers or waiving inspection contingencies to win a townhome in Henderson.

Clark County's median price per square foot stands at $252 as of September 2025, down 1.2% year-over-year. The median single-family home price hit $470,000, while condos sold for a median of $294,000—offering substantial price differentiation for those moving from larger homes to smaller footprints.

Homes now sit on the market an average of 45–56 days before selling, nearly double the 28-day median recorded in August 2024. This extended timeline gives sellers breathing room to prep, stage, and price strategically without the fear of "going stale" in a week.

According to the latest Las Vegas Realtors (LVR) market update, only 72% of single-family homes and 67% of condos and townhomes sold within 60 days in September 2025, compared to over 81% the previous year. Translation: Buyers are taking their time, conducting thorough inspections, and negotiating repairs—conditions that favor prepared sellers who understand the process.

Las Vegas Housing Inventory & Months of Supply Trend

2023–2025

8,000 6,000 4,000 2,000 0

5.0 4.0 3.0 2.0 1.0

4,000

4,500

5,500

7,502

2.0

1.8

2.6

4.0

Q1 2023 Q3 2023 Q1 2024 Sep 2025

Active Inventory (Units)

Months of Supply

Sources: Las Vegas Realtors (LVR) monthly reports, Clark County MLS data

Chart showing inventory levels and months of supply from 2023 through September 2025. Sources: Las Vegas Realtors (LVR) monthly reports, Clark County MLS data.

Top 4 Reasons Las Vegas Homeowners Downsize

1. Financial Strategy & Equity Liberation

Las Vegas homeowners who purchased before 2020 are sitting on substantial equity gains. With the median single-family home priced at $470,000, many sellers are unlocking $100,000 to $500,000+ in net proceeds after paying off existing mortgages and closing costs.

Henderson market data shows downsizers routinely reduce monthly housing costs by 30–50% through strategic moves to smaller homes. This reduction comes from four sources: lower utilities, reduced maintenance expenses, decreased insurance premiums, and smaller property tax bills.

All-cash purchases represented 23% of Las Vegas property sales in September 2025. Many of these transactions involved downsizers using equity from a previous home sale to eliminate mortgage payments entirely, freeing monthly cash flow for retirement, healthcare, travel, or investments.

2. Maintenance Reduction

A 2,800-square-foot home with a front and back yard requires ongoing attention: HVAC maintenance, exterior painting every 5–7 years, roof replacement, landscaping, pool service, and seasonal repairs. The time and financial commitment compounds over the years.

Downsizing to a condo or townhome shifts much of this responsibility to homeowners associations (HOAs). Landscaping, exterior maintenance, roof repairs, and community amenities become collective expenses managed by the HOA, freeing homeowners from weekend chores and contractor coordination.

Even single-story homes on smaller lots reduce maintenance burden significantly. Less square footage means fewer rooms to clean, less carpet to replace, and reduced HVAC runtime.

3. Lifestyle Optimization

Empty nesters and homeowners entering retirement often discover they're maintaining space they don't use. Guest bedrooms sit vacant 50 weeks a year. Formal dining rooms become storage areas. Home offices that once served school-age children now collect dust.

Downsizing removes unused square footage and redirects resources toward activities that enhance quality of life: travel, hobbies, dining, entertainment, healthcare, and time with family. Many downsizers report feeling "lighter" after eliminating the physical and mental weight of managing a large property.

Active-adult communities in Henderson offer resort-style amenities—pools, fitness centers, golf courses, walking trails, and social clubs—without the burden of personal ownership or maintenance. Residents access these benefits through HOA fees while living in right-sized homes.

4. Affordability & Tax Efficiency

Clark County maintains an effective property tax rate of approximately 0.65% of assessed value. While this is lower than many states, property taxes still scale with home values. Downsizing from a $470,000 home to a $350,000 condo reduces annual property taxes from roughly $3,055 to $2,275—a savings of $780 per year, or $65 monthly.

Nevada law caps annual property tax increases at 3% for primary residences, protecting long-term homeowners from dramatic tax spikes regardless of market appreciation. This stability is particularly valuable for those on fixed retirement incomes.

Home insurance costs also scale with property size and replacement value. The average homeowners insurance in Las Vegas is $1,393 annually ($116/month), while Henderson averages $1,188 annually. Smaller homes with lower replacement costs reduce premiums, often saving $50–$150+ per year.

Choose Your Next Home Type: A Comparison Guide

Downsizers in Las Vegas and Henderson have four primary property types to consider, each offering distinct advantages in price, maintenance, and lifestyle. Here you can read our opinion of Henderson and Summerlin New Construction or Resale. Thebrenkusteam.com

Property Type Comparison for Las Vegas Downsizers

Lowest Entry Price

Condo: $294K

Lowest Maintenance

Condo

Best Accessibility

Single-Story

Single-Story Homes

Las Vegas currently lists 2,643 single-story homes with a median listing price of $468,000. These properties offer the traditional homeownership experience—private yards, garages, and autonomy over property decisions—without the accessibility challenges of stairs.

Single-story homes are ideal for aging-in-place considerations. With all living spaces on one level, homeowners avoid stair-related mobility concerns that may emerge over time. Many buyers prioritize this feature even if current mobility is not a concern.

The tradeoff: Single-story homes require owner-managed maintenance. Yard work, exterior painting, roof repairs, and HVAC service remain the homeowner's responsibility. However, HOA fees are typically lower ($60–$150/month) compared to attached housing.

Townhomes

Henderson leads the region in new townhome construction, particularly within master-planned communities like Cadence, Inspirada, and Union Village. New construction townhomes range from $359,990 to $520,000, offering modern finishes, energy efficiency, and builder warranties.

Townhomes provide a middle ground between single-family homes and condos. Owners typically maintain interior spaces and small patios, while HOAs handle exterior maintenance (roofs, siding, landscaping) and community amenities such as pools, parks, and walking trails.

Most townhomes feature two levels, which may present accessibility considerations for some buyers. However, the reduced footprint—often 1,400–1,800 square feet—significantly lowers utility costs and cleaning time compared to larger single-family homes.

Condos

The Las Vegas condo market recorded a median sale price of $294,000 in September 2025, down 1.8% year-over-year. Henderson offers 179 condo units currently, with average prices around $350,000 in communities like Green Valley Ranch, Anthem, and MacDonald Highlands.

Condos deliver the lowest maintenance responsibility of any property type. HOAs typically cover all exterior work, structural repairs, roofing, landscaping, and shared amenities. Owners are responsible only for interior maintenance and improvements.

This full-service model comes with higher HOA fees—typically $200–$600+ monthly depending on building amenities, elevator service, concierge staff, and fitness facilities. For downsizers seeking a lock-and-leave lifestyle with minimal property management, condos offer unmatched convenience.

Many condo buildings provide elevator access, making them accessible for residents with mobility concerns. High-rise and mid-rise condos often feature security, covered parking, and resort-style amenities within walking distance of units.

Active-Adult (55+) Communities

Henderson is home to 23 active-adult communities, including major developments like Sun City Anthem (approximately 7,144 homes, prices $400,000–$1.2M+), Sun City MacDonald Ranch (from $350,000+), and Del Webb at Lake Las Vegas.

These neighborhoods are age-restricted (typically 55+) and feature resort-style amenities such as clubhouses, fitness centers, pools, golf courses, tennis courts, and 80+ social clubs. Residents access a full calendar of activities—from pickleball leagues to book clubs—without leaving the community.

The maintenance-free model is central to the appeal. Exterior landscaping, roof repairs, and community infrastructure are managed collectively through HOA fees, allowing residents to focus on lifestyle rather than property upkeep.

Prices vary widely based on home size, views, and community prestige. Entry-level active-adult homes start around $350,000 for attached housing, while premium single-family homes with golf course views can exceed $1 million.

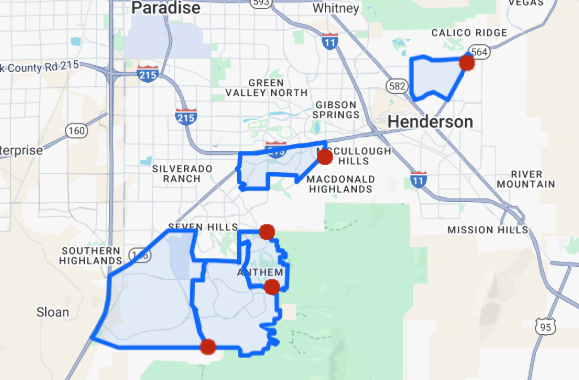

Map showing key Henderson areas for downsizers: Cadence (new construction townhomes and active-adult options), Inspirada (master-planned with diverse housing), Anthem (established with views and 55+ communities), Green Valley Ranch (central location with condos and townhomes).

The Financials: Equity, Costs, and Savings Breakdown

Using Your Equity for an All-Cash Purchase or Larger Down Payment

With Las Vegas' median single-family home at $470,000, homeowners who purchased years ago or paid down mortgages often hold $200,000–$400,000+ in equity. After accounting for payoff balances, closing costs, and any negotiated repair credits or compensation (all discussed in written agreements), many downsizers walk away with substantial net proceeds.

These funds can be deployed in multiple ways. Some buyers make all-cash offers on their next property, eliminating mortgage payments entirely. Others use large down payments (40–60% or more) to minimize monthly loan obligations and secure better interest rates.

All-cash transactions represented 23% of Las Vegas sales in September 2025. Cash buyers often negotiate stronger terms—shorter inspection periods, faster closings, or price reductions—because sellers value certainty and speed.

For homeowners carrying existing mortgages, selling first and using proceeds provides a clean financial break. Alternatively, bridge loans or home equity lines of credit (HELOCs) can provide temporary liquidity to purchase before selling, though these options carry higher costs and require careful planning.

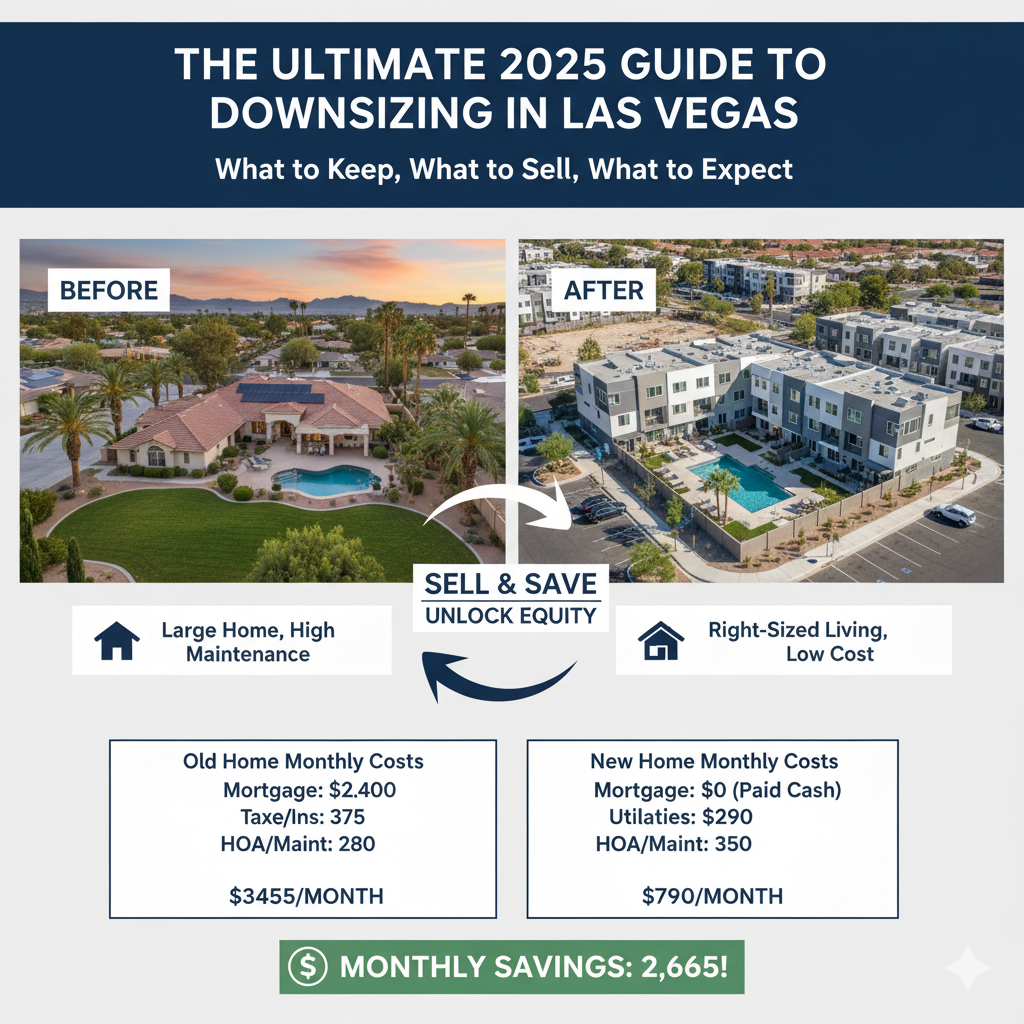

Monthly Cost Comparison: Before vs. After Downsizing

Understanding the full financial picture requires comparing all housing costs, not just mortgage payments. The table below illustrates estimated monthly expenses for a homeowner moving from a 2,800-square-foot single-family home to a 1,600-square-foot condo.

Monthly Cost Comparison: Downsizing Impact

2,800 sq ft Single-Family Home → 1,600 sq ft Condo

BEFORE Downsizing

2,800 sq ft Home

Mortgage* $2,400

Utilities $400

Property Taxes $250

Insurance $125

HOA Fees $80

Maintenance $200

Monthly Total

$3,455

AFTER Downsizing

1,600 sq ft Condo

Mortgage* $0

Utilities $150

Property Taxes $190

Insurance $100

HOA Fees $350

Maintenance $0

Monthly Total

$790

💰 Total Monthly Savings

$2,665

That's $31,980 saved annually

Where the Savings Come From

Mortgage Elimination $2,400

Utilities $250

Maintenance $200

Property Taxes $60

Insurance $25

⚖️

Trade-off: HOA Increase

HOA fees increase by $270/month, but this covers all maintenance, landscaping, exterior repairs, and amenities.

*Mortgage amounts vary significantly based on loan terms, interest rates, down payments, and purchase timing. These figures illustrate a calculation method, not financial advice. Your actual costs will differ based on your specific circumstances. Consult a licensed lender and financial advisor for personalized analysis.

Key insights from this comparison:

-

Utilities drop sharply in smaller spaces due to reduced heating/cooling requirements and shared walls in attached housing.

-

Property taxes scale with assessed value; downsizing to a less expensive property reduces this fixed cost.

-

HOA fees increase in full-service buildings but eliminate owner-paid maintenance, landscaping, and exterior repair costs.

-

Insurance premiums decline with lower replacement values.

The net result: Many downsizers achieve $2,000–$3,000 in monthly savings even after accounting for higher HOA fees, freeing cash flow for discretionary spending, healthcare, or savings.

Clark County Property Tax Cap Explained

Clark County property taxes are capped by Nevada law (NRS 361.4722) at a 3% annual increase for primary residences, regardless of how rapidly assessed values rise. This protection ensures predictable, manageable tax growth over time.

The effective property tax rate in Clark County is approximately 0.65% of assessed value. For example, a $350,000 condo generates roughly $2,275 in annual property taxes ($190/month). Even if the condo appreciates to $400,000 over five years, the tax increase is limited to 3% per year on the original assessed value, not the full market appreciation.

For downsizers living on fixed incomes, this cap provides critical budget stability. Review current tax rates and payment schedules at the Clark County Treasurer's Tax Rate portal.

Home Insurance & Utility Cost Realities

The average cost of homeowners insurance in Las Vegas is $1,393 per year ($116 monthly), while Henderson averages slightly lower at $1,188 annually. Insurance premiums vary based on location, coverage amounts, deductibles, and claims history.

Smaller properties with lower replacement costs reduce insurance premiums. A 1,600-square-foot condo requires less coverage than a 2,800-square-foot single-family home, often saving $50–$150+ annually.

Nevada insurance rates increased in 2025 due to natural disaster risks (flash floods, earthquakes, wildfires) and rising construction costs, affecting homeowners across all property types.

Utility costs—including electricity, water, waste, and heating—average $190–$250 monthly in standard Las Vegas homes. Condos and townhomes with shared walls, smaller square footage, and energy-efficient construction often reduce these costs by $200–$400 monthly, particularly during extreme summer and winter months when HVAC systems run continuously.

Resale vs. New Construction in 2025: What Downsizers Need to Know

Both resale homes and new construction offer advantages for Las Vegas downsizers. The optimal choice depends on priorities: move-in readiness versus modern features, established neighborhoods versus new amenities, and immediate possession versus construction timelines.

Resale vs. New Construction: 2025 Comparison for Downsizers

Which option fits your timeline, budget, and lifestyle?

🏡 Resale Home

Established & Move-In Ready

✓ PROS

- Move-in ready – no waiting

- Mature landscaping, established neighborhoods

- Often lower price per sq ft

- Shorter closing timelines (30–45 days)

⚠ CONS

- May need updates, repairs, or staging

- Limited warranties (sold as-is unless negotiated)

- Older HVAC, appliances, roofing nearing replacement

💡 2025 INCENTIVES

- Seller concessions for repairs/closing costs

- Longer inspection periods due to inventory levels

- More negotiating power on price and terms

🏗️ New Construction

Modern & Builder Incentives

✓ PROS

- Modern finishes, energy efficiency

- Builder incentives (rate buydowns, closing credits, upgrades)

- Warranties (1-year workmanship, 10-year structural)

- No immediate repairs needed

⚠ CONS

- Construction delays possible

- HOA fees often higher in new communities

- Less mature landscaping

- Lot premiums for views/corner locations

💡 2025 INCENTIVES

- Rate buydowns (2-1 or 1-0 temporary reductions)

- $10K–$25K+ in design center credits

- Paid HOA dues for first year

- Closing cost assistance up to 3–5%

Quick Decision Guide for Downsizers

Choose Resale If...

- You need to move within 30–60 days

- You prefer established neighborhoods close to amenities

- You want mature landscaping and character

- You're willing to negotiate repairs or credits

Choose New Construction If...

- You can wait 4–6+ months for completion

- You want modern finishes and energy efficiency

- You value builder warranties and no immediate repairs

- You want to leverage rate buydowns and incentives

2025 Market Insight

Both options benefit from 4+ months of supply and slower market conditions—giving downsizers negotiating power and time to make informed decisions.

Are Builder Rate Buydowns Worth It?

Builders in Las Vegas and Henderson are offering aggressive incentives in 2025 to move inventory amid slower sales. One popular incentive is the temporary interest rate buydown.

A 2-1 buydown reduces your mortgage rate by 2% in Year 1 and 1% in Year 2, then reverts to the original rate in Year 3. For example, if the market rate is 6.5%, you'd pay 4.5% in Year 1, 5.5% in Year 2, and 6.5% thereafter.

This lowers initial monthly payments, making homes more affordable in the short term. However, it's not a permanent rate reduction. Evaluate whether you'll refinance within two years (if rates drop) or can afford the full payment starting in Year 3.

In some cases, negotiating a price reduction instead of a buydown delivers better long-term value. Price reductions reduce principal, property taxes, and interest paid over the life of the loan. Discuss both options with your lender.

Warranty & Repair Tradeoffs

New construction homes include builder warranties: typically 1 year for workmanship defects, 2 years for systems (HVAC, plumbing, electrical), and 10 years for structural issues. This coverage provides peace of mind and reduces repair costs in early ownership.

Resale homes are generally sold as-is unless buyers negotiate repair credits or seller concessions during the inspection period. Smart buyers request a pre-listing inspection or home warranty (costing $500–$700 annually) to cover appliances, HVAC, and systems for the first year.

With 4+ months of housing supply and longer market times, resale home buyers in 2025 have leverage to request repairs, price reductions, or closing cost credits. Sellers motivated to close often agree to reasonable inspection requests rather than re-list and wait another 45–60 days.

Process Map: Sell, Buy, and Move Without Chaos

Downsizing involves coordinating two major transactions—selling your current home and purchasing your next—while managing decluttering, packing, and moving logistics. A clear process map prevents overlap, stress, and costly mistakes.

Step 1: Prep & Stage Your Current Home

Start by decluttering room-by-room (see "What to Keep, What to Sell, What to Donate" below). Removing 30–40% of furniture, personal items, and décor makes spaces appear larger and allows buyers to envision their own belongings in the home.

Address obvious repair needs before listing: HVAC service, plumbing leaks, roof condition, and any deferred maintenance that could raise red flags during buyer inspections. Small repairs now prevent larger concessions later.

Professional staging focuses on maximizing natural light, neutralizing décor, and highlighting the home's best features. In a market with 45–56 average days on market, proper preparation pays dividends in faster sales and stronger offers.

Timeline: Allocate 3–6 weeks for prep, repairs, and staging before listing. Current market conditions allow adequate time without rushing.

Step 2: List Timing & Pricing Strategy

With over 4 months of housing supply, Las Vegas Realtors (LVR) data shows that pricing competitively is critical. Overpriced homes sit longer, accumulate days on market, and eventually require price reductions—creating a perception of distress or defects.

Use a comparative market analysis (CMA) based on recently closed sales (not active listings) in your neighborhood. Homes that sell within 30–45 days are typically priced within 2–3% of true market value.

Spring (March–May) and fall (September–November) traditionally see higher buyer activity in Las Vegas, though 2025's elevated inventory means homes sell year-round for sellers who price correctly and present well.

Step 3: Contingencies, Rent-Backs & Simultaneous Closings

Coordinating two transactions requires strategic contract terms. Three common approaches:

Home sale contingency: Make your purchase offer contingent on successfully selling your current home. In balanced markets, sellers are more willing to accept these contingencies than during competitive conditions. Build in reasonable timelines (60–90 days) and escalation clauses if your home sells quickly.

Rent-back agreements: Negotiate to stay in your sold home for 30–60 days post-closing while finalizing your next purchase. Rent-backs are often structured at a daily rate equal to the buyer's carrying costs (mortgage, taxes, insurance divided by 30). This eliminates double moves and temporary housing.

Bridge loans: Short-term financing allows you to purchase your next home before selling your current property. Bridge loans carry higher interest rates and fees but provide flexibility in competitive scenarios. Most lenders require 20–30% equity in your current home to qualify.

Discuss these options with your real estate professional and lender early in the process. Compensation for real estate services is negotiable and discussed in written buyer and listing agreements.

Step 4: Inspection, Repairs & Negotiation

Expect a 10–14 day inspection period once you're under contract. In 2025's balanced market, buyers have leverage to request repairs, price reductions, or closing cost credits for issues discovered during inspection.

Common requests include HVAC repairs, plumbing fixes, roof repairs, electrical updates, and pest treatment. Sellers can respond by completing repairs, offering credits at closing, or reducing the purchase price.

Set aside 1–2% of your sale price for unexpected repair requests or concessions. While not all buyers will request major repairs, having a contingency budget prevents surprises.

For your own purchase, conduct thorough inspections of your next home—whether resale or new construction. Inspection periods are negotiable; use the time to identify any issues before committing.

Local Rules & Resources: What You Need to Know

Clark County Zoning Updates (October 2025)

If you've read our blog 'What Clark County's Latest Zoning Changes Mean for Homebuyers and Sellers in 2025'. On October 22, 2025, the Clark County Comprehensive Planning Department approved significant zoning map amendments affecting residential development across unincorporated areas. thebrenkusteam.com

Key changes include:

-

RS-20 to RS-2 conversions in Enterprise: Minimum lot sizes reduced from 20,000 square feet to 2,000 square feet—a tenfold density increase.

-

Indian Springs density transformations: RS-40 to RS-5.2 zoning creates nearly five times more homes on the same acreage.

-

Master Plan amendments: Shifts from "Mid-Intensity Suburban" to "Compact Neighborhood" designations in multiple areas.

-

Updated overlay districts: Changes to Rural Neighborhood Preservation (RNP) and Red Rock Overlay District standards.

For downsizers, these zoning changes signal expanded future inventory of smaller-lot single-family homes, townhomes, and attached housing in suburban corridors. While maintaining single-family character, higher-density zoning accommodates growth through more compact development patterns.

Review the full zoning code and recent map amendments at Clark County Comprehensive Planning's zoning information portal.

Nevada Housing Division Programs (Neutral Overview)

The Nevada Housing Division (NHD) administers several homebuyer assistance programs, primarily targeting first-time buyers and income-qualified households. However, some programs are available to repeat buyers, including downsizers who meet eligibility criteria.

Home Is Possible: Offers up to 5% of the loan value for down payment or closing costs. Available to both first-time and repeat buyers with household incomes below $165,000 and home purchase prices at or below $806,500. This program uses income and price limits that adjust periodically; verify current thresholds before applying.

Home Is Possible for First-Time Homebuyers: Provides up to 4% of the loan amount as an interest-free second mortgage for down payment and closing costs, repaid over 30 years. Requires a 640 minimum credit score and completion of homebuyer education. Restricted to first-time buyers only.

Mortgage Credit Certificate (MCC): A federal income tax credit allowing first-time buyers and qualified veterans to claim up to 30% of annual mortgage interest paid as a tax credit (not deduction). This can save thousands annually, effectively reducing borrowing costs.

Home First: Offers up to $15,000 in forgivable down payment assistance (forgiven after three years) for first-time buyers who have been Nevada residents for at least six months.

Most NHD programs prioritize first-time buyers or households below area median income. Repeat buyers have limited options, with Home Is Possible being the primary program available to downsizers who meet income and price requirements.

Explore eligibility and apply at Home Is Possible NV. The division partners with 50+ approved lenders throughout Nevada.

What to Keep, What to Sell, What to Donate: The Downsizing Decision Framework

Transitioning from a large home to a smaller space requires intentional decisions about possessions. The goal: keep items that serve current needs and bring joy; eliminate duplicates, unused items, and anything maintained out of guilt or obligation.

Room-by-Room Checklist

Living/Family Rooms:

-

Keep: 1 sofa, 2 chairs, essential media console, 1–2 side tables, lighting

-

Sell: Oversized sectionals, duplicate furniture, bulky entertainment centers, extra coffee tables

-

Donate: Unused décor, books you won't re-read, outdated electronics, excess throw pillows/blankets

Kitchen:

-

Keep: Everyday dishes (service for 4–6), 1 set cookware, essential small appliances (coffee maker, toaster, blender), everyday glassware

-

Sell: China sets, silver service, specialty appliances (bread makers, fondue sets, pasta makers), duplicate utensils

-

Donate: Extra glassware, serving platters used once annually, cookbooks (digitize favorites), mismatched containers

Bedrooms:

-

Keep: Bed, 1 dresser, 1 nightstand per person, essential clothing (current season + 1 year unworn maximum)

-

Sell: Guest bedroom furniture sets, extra mattresses, large armoires, oversized dressers

-

Donate: Linens (keep 2 sets per bed), clothing unworn in 12+ months, old pillows, excess hangers

Garage/Storage:

-

Keep: Seasonal items you actually use, tools for basic repairs, holiday décor (limit to favorites)

-

Sell: Power tools, lawn equipment (if moving to HOA-maintained property), sports gear, exercise equipment

-

Donate: Holiday décor overload, camping equipment unused in 3+ years, boxes of "someday" projects, duplicates of anything

Sentimental Items Framework

Sentimental items present the greatest downsizing challenge. A structured approach prevents paralysis:

Digitize when possible: Scan photos, children's artwork, awards, certificates, and documents. High-resolution scans preserve memories without physical storage. Services like Legacy Box convert old videos, slides, and film to digital formats.

One-box rule: Limit memorabilia to one clearly labeled container per family member. If it doesn't fit in the box, evaluate whether it's truly irreplaceable or simply familiar.

Pass-on conversations: Offer heirlooms, family furniture, and sentimental items to adult children or relatives before moving. Don't assume they want items—ask directly and respect their decisions. Many adult children live in smaller spaces themselves and cannot accommodate large furniture or collectibles.

Professional services: Estate sale companies, senior move managers, and professional organizers specialize in downsizing logistics. Donation pickup services from Goodwill, Salvation Army, and Habitat for Humanity ReStore handle large furniture and household goods, providing tax deduction receipts for charitable contributions.

FAQs About Downsizing in Las Vegas (2025)

Q: Is 2025 a good year to downsize in Las Vegas?

A: Yes. With over 4 months of housing supply, stabilizing prices, and increased inventory of condos, townhomes, and single-story homes, downsizers have more options and negotiating power than in the competitive seller's market of 2021–2023. Longer market times (45–56 days average) allow proper preparation and strategic pricing without rushed decisions.

Q: How much are HOA fees in Henderson 55+ communities?

A: HOA fees in Henderson's active-adult communities range from $200 to $600+ per month, depending on amenities and services. Full-service communities with golf courses, fitness centers, multiple pools, and clubhouses charge higher fees but cover landscaping, exterior maintenance, and extensive recreational programming. Standard townhome and condo HOAs in non-age-restricted communities typically range $150–$350 monthly.

Q: What is the property tax cap in Clark County, Nevada?

A: Nevada law (NRS 361.4722) caps annual property tax increases at 3% for primary residences, regardless of how much assessed values rise. Clark County's effective property tax rate is approximately 0.65% of assessed value. This cap provides budget predictability, especially for homeowners on fixed retirement incomes.

Q: How do I use my home equity for a down payment on my next home?

A: You can access equity in several ways: (1) Sell your current home first and use net proceeds for your next purchase—the cleanest approach; (2) Open a home equity line of credit (HELOC) before selling to access funds for a down payment; (3) Use a cash-out refinance to convert equity to cash; (4) Obtain a bridge loan for temporary financing until your home sells. Consult with a licensed lender to evaluate costs, rates, and timing for your specific situation.

Q: Can I get down payment assistance if I'm not a first-time buyer?

A: Yes, but options are limited. The Nevada Housing Division's "Home Is Possible" program offers up to 5% assistance for repeat buyers who meet income limits (household income under $165,000) and purchase homes priced at $806,500 or less. Most other state and local assistance programs target first-time buyers exclusively. Check current program details at Home Is Possible NV.

Next Steps: Your Downsizing Action Plan

Downsizing in 2025's Las Vegas market combines opportunity with preparation. You have the inventory, the equity, and the market conditions to make a strategic move that reduces costs, simplifies lifestyle, and positions you for the next chapter.

Start with the numbers: Calculate your current home's likely net proceeds, estimate monthly costs for your target property types, and identify your non-negotiable features (single-story access, specific neighborhoods, amenity priorities).

Tour properties across multiple categories—single-story homes, townhomes, condos, and active-adult communities—to understand what resonates with your lifestyle and budget. Don't assume you know which property type is right until you've experienced the differences firsthand.

Connect with professionals early: Real estate agents familiar with downsizing transactions, lenders who can pre-qualify you and explain financing options, and estate sale or moving companies if you need logistical support.

Curious how these numbers apply to your situation? Let's connect and explore your options. Whether you're ready to list tomorrow or planning for next year, a conversation costs nothing and clarifies everything.

About the Author

Gavin Brenkus | Lead Agent & Director of Lead Generation

A three-time recipient of the prestigious "Who's Who Under 40" award from Las Vegas REALTORS®, Gavin Brenkus has firmly established himself as one of the most accomplished real estate professionals in Southern Nevada. As a Lead Agent and the Director of Lead Generation for The Brenkus Team, he is an integral part of a family-owned legacy that has achieved nearly $2 billion in sales volume and successfully closed over 8,000 transactions.

For Gavin, real estate is more than a profession—it's a lifelong passion. Immersed in the industry from the age of 16 and licensed before graduating high school, he offers a rare depth of market knowledge that combines youthful energy with decades of absorbed expertise.

His professional philosophy is built on a foundation of listening. Gavin is dedicated to fully understanding the unique wants and concerns of his clients, allowing him to curate a tailored and seamless experience from start to finish. This client-first approach ensures that everyone he works with feels heard, valued, and expertly guided.

Disclaimer: This guide is for informational purposes only and does not constitute financial, tax, or legal advice. Market data, prices, inventory levels, and program details are subject to change. Compensation for real estate services is negotiable and is discussed in written buyer representation and listing agreements between clients and brokers. Consult qualified professionals—including licensed real estate agents, mortgage lenders, tax advisors, and attorneys—before making real estate or financial decisions. All figures, cost estimates, and savings calculations presented are examples for illustration purposes and will vary based on individual circumstances, market conditions, property characteristics, and financing terms.

|

or another way