Categories

Costs, BuyingPublished August 15, 2025

What Fees Are Involved with Buying a Home in Las Vegas?

What Fees Are Involved with Buying a Home in Las Vegas?

It starts with a dream! Until reality sets in. You want to buy a home in Las Vegas (Clark county, NV area) then you aren’t sure what the fees are and because you are not sure what to expect for your budget we find most people give up before the process starts.

As Realtors® and educators, The Brenkus Team believes in having the heart of a teacher with all things Real Estate. We use this article to give you the clarity you need to take action now and feel comfortable and confident with what happens next.

You’ll find that buying a home in Las Vegas involves more than the purchase price. There are one-time fees at closing, some costs set by law, others that vary, and ongoing expenses once you move in. This article breaks down; mandatory costs, optional/negotiable costs, hidden costs, budgeting tips, and reflects typical 2025 practices in Nevada and Clark County.

Quick overview

Most purchasers will pay a mix of lender fees (like origination and appraisal), settlement costs (like escrow, title insurance, recording, and transfer tax), plus insurance and prepaid items collected at closing.

Actual amounts vary by loan program, property type, and provider.

Nevada also has state and county specific rules that affect certain items. For example, Real Property Transfer Tax (RPTT) and recording fees. Seller usually will pay for this on a Previously owned property. You may be asked to pay this if you buy a new construction home.

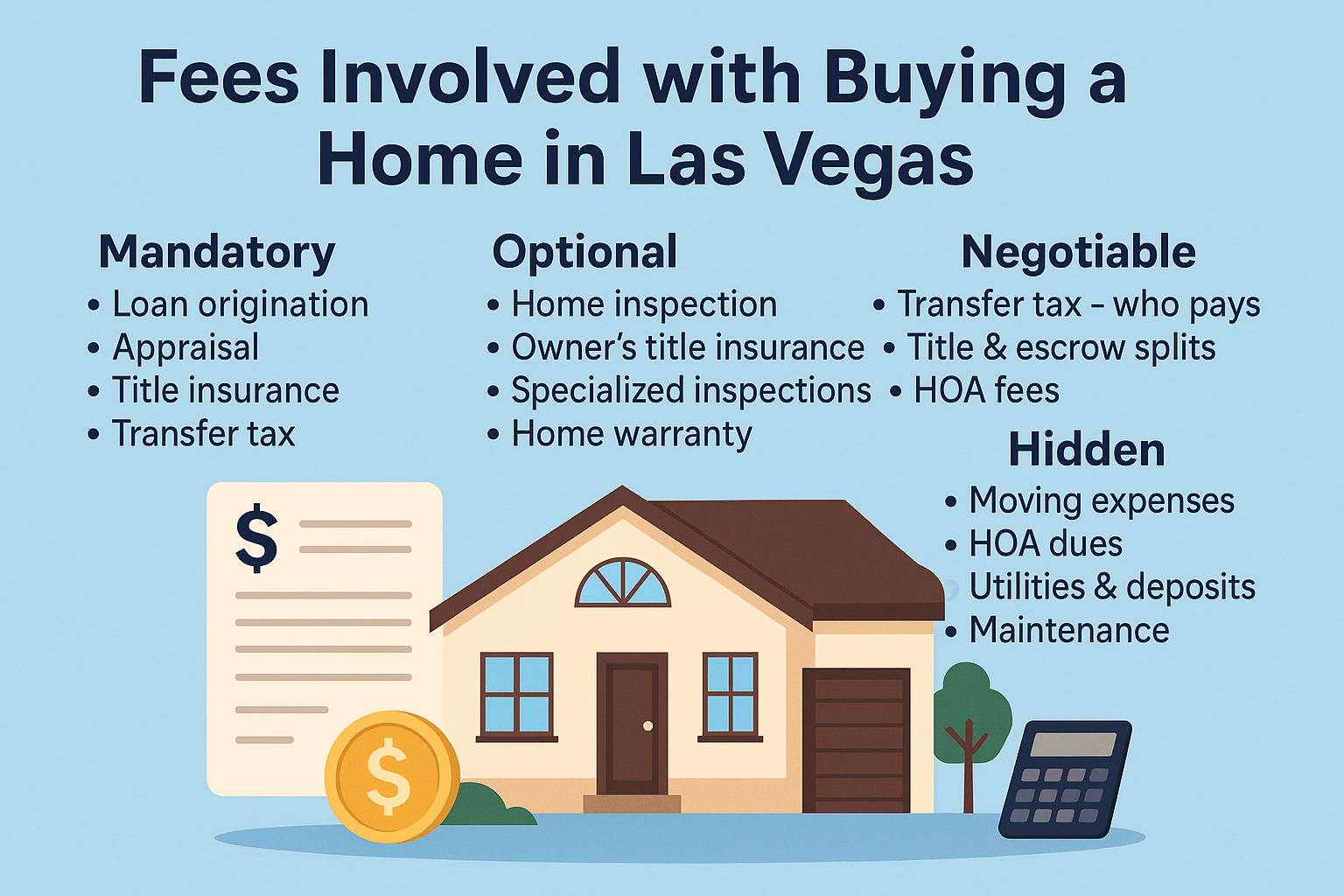

Mandatory costs most purchasers should expect

These are generally required by lenders, state or local law, or common industry practice when using a mortgage.

-

Loan origination fee

Charged by lenders for processing and underwriting the loan.

Commonly 0.5%–1% of the loan amount (e.g., $2,000–$4,000 on a $400,000 loan).

This will be shown on your standardized Loan Estimate and Closing Disclosure. -

Appraisal

Required by most lenders to confirm the home’s value.

Typical costs in Nevada are $400–$700+, depending on property size and complexity. -

Lender’s title insurance policy

Protects the lender’s interest in the property.

Nevada title insurance rates are regulated—insurers must file them with the Division of Insurance.

Buyers can use public title company calculators to get estimates. -

Escrow/settlement services

A neutral escrow company manages funds and documents.

Fees vary by provider and transaction type; you can obtain estimates using the same calculators. -

County recording

Clark County charges $42 per standard document under NRS 247.305 and county ordinance. Certain documents may have different amounts. -

Nevada Real Property Transfer Tax (RPTT)

Clark County rate: $5.1 per $1,000 of value (about 0.51% of the sale price). -

Example $500,000 home / $1,000 = 500. 500 * 5.1 = $2,550

-

In resales, it’s often seller-paid; with some new builds, the builder may require the buyer to pay.

-

Homeowners insurance (first year cost)

Lenders require proof of homeowners insurance, with the first year’s cost often collected at closing. Nevada’s average annual cost is generally $1,100–$1,500+, depending on coverage and location. -

Prepaid items (property taxes and interest)

Covers interest from your closing date through month-end and typically 2–6 months of property taxes to set up an escrow account. Example: If you close on August 20, you may prepay interest for August 20–31 and contribute several months of property taxes. -

Private Mortgage Insurance (PMI), if applicable

Conventional loans with less than 20% down typically require PMI.

Costs are often 0.5%–1% of the loan amount per year, paid monthly until you meet cancellation criteria. FHA and VA loans have different insurance structures (MIP or funding fees).

Optional but smart (and sometimes negotiated)

Not legally required, but often used for added protection.

-

Home inspection

We recommended Home inspections to assess property conditions. What comes back on the home inspection could save you money in a Negotiation. Las Vegas pricing is $350–$700, varying with size and add-ons -

Owner’s title insurance policy

Protects your ownership interest. Not mandatory in Nevada, but commonly included in resale transactions for buyer protection. Rates are regulated; estimates available via public title company calculators. (most of the time paid by seller and depends on the cost of home) -

Specialized inspections

Inspections may be advisable depending on the property.Here are some examples. Pool $200, pest/termite $100 structural $500 -

Home warranty

A one-year plan covering certain systems/appliances; prices vary by provider and coverage level.Cost depends on size of home and coverages of features of appliances. $450 -1500

Negotiable or situational costs

These fees may be assigned to either party depending on the contract and market conditions.

-

Owner’s title insurance & escrow splits

We find the seller pays the owner's title, and escrow fees are split 50/50, but this is negotiable. This depends on the cost of home and Escrow company. -

HOA transfer-related fees (if in a common-interest community)

Nevada law controls what can be charged for resale packages and transfer fees.

Buyers have a five-calendar-day right to cancel after receiving the resale package (weekends and holidays included unless otherwise stated).

Overlooked costs after closing

Not always on the first estimate, but they can affect your budget in the first year.

-

Moving and setup – Trucks, movers, packing materials, lock changes, and window coverings.

-

Monthly HOA dues and special assessments (if applicable) – Dues vary widely; special assessments are possible. Review the resale package for current dues and any planned projects.

-

For example, as of 2025 Cadence has a payable quarterly at $225 per quarter and Heritage HOA (a Sub‑Association) $175 per month

-

Utilities and deposits – Some providers require deposits or activation fees.

-

Maintenance and repairs – Plan for routine servicing and unexpected fixes.

-

Supplemental insurance – Flood or earthquake coverage may be advisable depending on the property’s location and your preferences.

Tips for budgeting and avoiding surprises

-

Interview a Realtor®

Realtors® like The Brenkus Team meet with hundreds of home buyers every year. We make personalized cost sheets for every buyer we meet with you can get yours for free HERE -

Use your Loan Estimate as your baseline

Lenders will give you their estimate within three business days of a completed application. Compare at least two lenders for differences in rates, fees, and third-party costs. Start with who your Realtor® recommends because you may get exclusive offers of savings. -

Verify transfer tax and recording amounts

Typically you wont pay for this on a resale home unless you negotiated to do so. If you are, check official Clark County and Nevada sources for current rates or ask your Realtor®. -

Get title/escrow quotes from more than one provider

Public calculators from major title companies help you compare costs before negotiating. -

Read the HOA resale package promptly (if applicable)

You have five calendar days after receipt to cancel based on the HOA documents. Review dues, rules, budgets, reserves, and future projects. -

Shop homeowners insurance early

Compare multiple quotes with the same coverage limits and deductibles.

City-level rates, including Las Vegas, can differ from state averages. -

Plan for move-in and the first year

Set aside funds for moving, deposits, small upgrades, and maintenance.

Fair-housing and compliance note

The fees and practices described here apply equally to anyone purchasing property in Las Vegas. They are presented in neutral, fact-based terms. When in doubt, rely on standardized documents (Loan Estimate, Closing Disclosure) and public Nevada or Clark County sources for official rates and timelines. Or Interview a Realtor® for a personal Itemized breakdown.

Bottom line

In Las Vegas, mandatory items are generally set by lenders and law—such as loan origination, appraisal, lender’s title, escrow/settlement, recording, transfer tax, insurance, and prepaid items. Optional protections like inspections and owner’s title insurance are common and can be worth the investment. Some costs are negotiable between buyer and seller, and a few after-closing items can affect your first-year budget. By getting firm quotes, reading every disclosure early, and keeping a cushion for the unexpected, you can walk into closing with confidence and fewer surprises.

Disclaimer: This blog is for general informational purposes only and does not constitute legal, financial, or tax advice. Always consult a licensed Nevada real estate professional (The Brenkus Team), lender, or attorney for guidance specific to your situation.

|

or another way